Drivers of industrial decarbonisation

High on the energy transition agenda is the need to reduce the environmental impact and emissions from carbon intensive industries. Energy, heat production and industrial processes account for 55% of all global greenhouse gas emissions.

National emissions targets

At the Paris Agreement in 2015, governments acknowledged that their national climate targets at the time would not meet the goal of limiting global warming to 1.5˚C. 2020 was the target year to submit long-term strategies and for emissions to reach a peak.

Consensus is that the progress made since 2015 has not been enough and an unprecedented effort is required by countries to cut levels of emissions and get back on track. Individual countries are adjusting their regulatory landscape to meet emissions target commitments and a growing number of governments have also set mid-century net-zero targets.

Carbon pricing

The World Bank estimates that carbon pricing schemes now cover about half of the emissions for regions that use such mechanisms.

Emissions do and will continue to increasingly impact the balance sheet with the growing development of carbon pricing, whether through emissions trading systems or carbon taxes. The objective here is to shift the burden onto emitting operators and developers. A carbon price also stimulates clean technology and market innovation, fuelling new, low-carbon drivers of economic growth.

Operational efficiency and optimisation

45% of decarbonisation goals can be tackled through better adoption of a circular economy.

Resolving repeat failures that cause process trips or shutdowns, stopping flaring and venting, ensuring operating parameters have not moved significantly from original efficiency levels, as well as finding and fixing asset-integrity issues that contribute to fugitive emissions are not just emission mitigation solutions, but offer substantial cost efficiencies and potential monetisation opportunities for surplus power or captured gas.

Investment proposition

95% of fund managers see international oil companies that are not responding to climate change-related risks as unattractive investments.

In recent years mainstream investors are following ethical investment groups in adopting criteria that excludes organisations and commodities groups based on hydrocarbon extraction and levels of carbon emissions. Furthermore, commitments sought include not only hard targets to reduce extraction and production emissions but also ‘indirect' or Scope 3 emissions from customers of their feedstock and products.

Licence to operate

Through the United Nations Sustainable Development Goals over 170 organisations have committed to reach net zero by 2050.

The public face of business visibility is also moving a pace with a greater emphasis on environmental, social and governance goals and contributions. The sustainability and societal impact of an investment is being increasingly scrutinised, and we are seeing major emitters announce carbon reduction and ambitious net zero targets on a regular basis.

Challenges, complexities and vulnerabilities

A continually evolving landscape and suite of interrelated societal, economic and commercial complexities present challenges to reducing emissions.

Ageing assets

Companies are risking $2.2trn by 2030 if they base investments on current emissions policies during the low carbon transition.

Older assets face more complex challenges in reducing emission intensity, it is often less efficient and logistically and economically challenging to replace or revamp. They contribute to fugitive emissions as parts fail or degrade. With ageing assets, there are multiple opportunities that can help drive significant improvements. As well as environmental benefits, a stronger level of governance around emissions also makes compelling commercial sense.

Asset footprint

It will be a necessity to examine geography and geopolitics to reduce exposure to potentially stranded assets.

Global industrial corporations are making enterprise-wide commitments to emissions, but their production and processing assets vary greatly in their geographic locations, both in terms of numbers but also scale of operations. Furthermore, there is a differing range of regulatory and legislative requirements within the relevant country or region.

Cost and subsidies

The removal of subsidies is expected to increase the installed capacity of renewables and the use of renewables in electricity by making these technologies cost competitive.

The speed of development and cost reductions within the low-carbon sector has benefited from government and regulatory support. This is as a result of legislation on the pricing of carbon emissions from fossil fuels and subsidies for alternative technologies for energy generation. It is expected that fossil fuel subsidies will be phased out meaning carbon intensive operations are not able to access subsidies in the way they have been able to.

Pandemic

The current COVID-19 pandemic is having a debilitating impact on the global economy.

With a significant drop in GDP and major impact on capital expenditure in the short term. There is increasing focus on financing future projects on greener, more resilient and sustainable solutions. This is coupled with a need for existing assets to be secure, resilient and producing at optimal levels. Alongside decarbonisation options, many industrial facilities will likely see a reduction in other harmful emissions positively impacting on air quality.

Pace of innovation

Existing infrastructure has been built over many decades to support conventional energy uses. The rapid transition to a decarbonised system will have implications for existing infrastructure.

The pace of innovation and technological solutions have a major part to play in decarbonisation, from the technologies to generate and deliver new energy sources to the digital innovations that will transform how we use them. Leveraging data and digital technology also offers a less capital-intensive route to optimise operational performance, target energy production and minimise waste

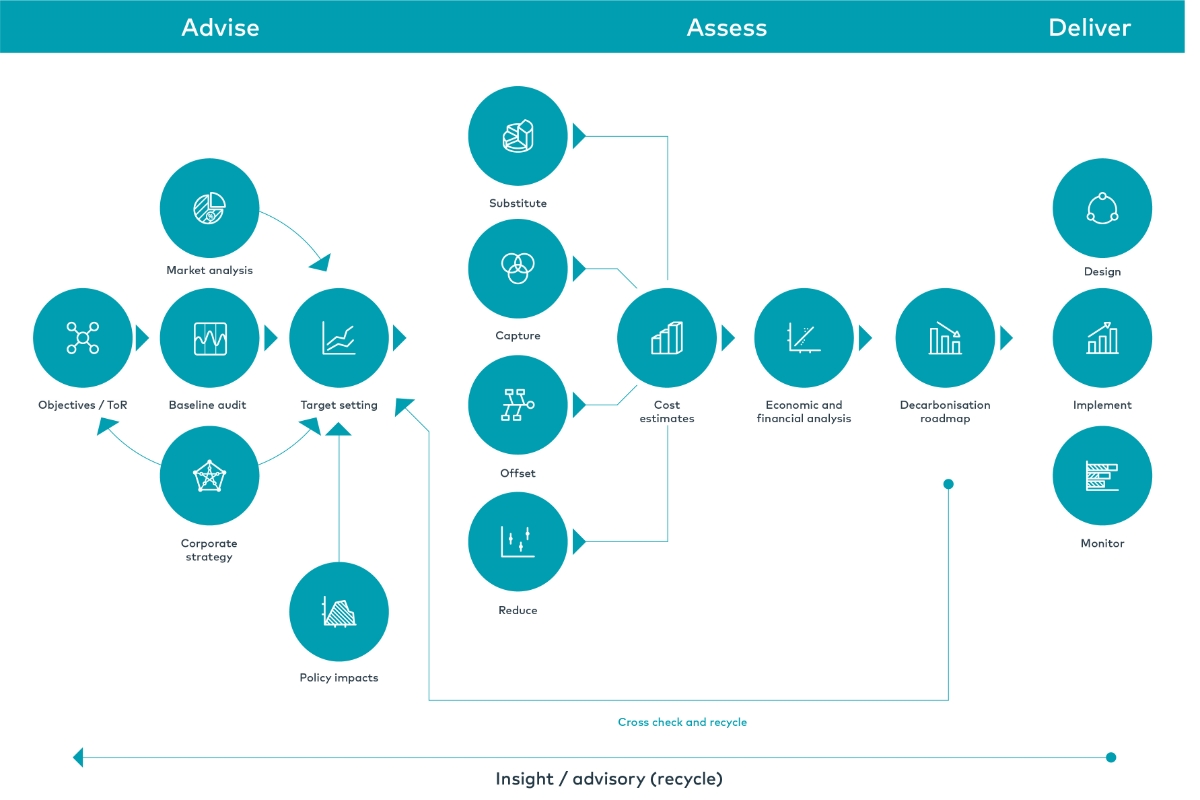

What’s your decarbonisation SCORE?

Operators and developers need to map their journey to decarbonised assets.

You need to fully understand policy landscape and the carbon baseline, before defining objectives and targets for decarbonisation through benchmarking, assessing market impacts and taking consideration of policy and corporate strategy. Then review and map assets to enable development of decarbonisation pathway scenarios.

As part of a wider delivery model, a SCORE screening process can be applied to single or multiple assets, to a client’s full asset portfolio or across a specific geography or region using an evaluation assessment of opportunities to:

Substitute -substitution of fuel or feedstocks consumed for renewable or less intensive sources. For example, switching electricity provision to a renewable source or considering use of renewable and bio feedstocks.

Capture - employing carbon capture technologies, or emissions control technologies, to substantially reduce or eliminate harmful emissions to the atmosphere.

Offset - considering assets or product portfolios across a country or company-wide scale to achieve decarbonisation/clean air goals.

Reduce - looking at holistic asset optimisation considering areas around energy efficiency, digitalisation and operations and maintenance best practise.

Evaluate - whatever your decarbonisation journey, it’s important to apply a structured evaluation process to be able to map out your decarbonisation journey to meet goals and lead to a successful outcome.

Understand the opportunities

The pathway to reduce the carbon emissions of extractive and process industries will need to leverage a breadth of solutions and will be bespoke to particular geographies, enterprise portfolios and individual assets.

Integrate renewables

Renewables are increasingly being integrated into industrial process operations worldwide. In Russia, Gazprom Neft is embarking on a project to build solar-power electricity plants at its refining facilities. Shell has installed one of the largest solar parks in the Netherlands at their Moerdijk Chemical Plant. In upstream oil and gas, platforms in the North Sea have introduced renewable power sources. Opportunities also exist for operators to supply power to third parties.

Optimise process and energy efficiency

Looking at process optimisation is key within the business model to ensure operators are able to maximise throughput and efficiency across their operations. This is inter-related with the selection of technology and practises to ensure energy efficient design. For example, minimising waste streams and energy leakage, throughout all aspects of process delivery and operations.

Detect and repair leaks

Leaking equipment is the largest source of emissions of carbon dioxide and air pollutants from oil and gas processing, refineries, and manufacturing facilities. Digital solutions can enhance the detection, asset integrity and response implementation with significant impact on emissions and reducing product losses, as well as increasing safety for the workforce and surrounding community.

Replace feedstock

Operators can consider other feedstocks over petroleum and natural gas, alternatives like biofuels present opportunities for production and use. Replacing or supplementing traditional fossil feedstocks with bio-based alternatives will reduce emissions. This is a developing area where technology is largely based around biofuels, biomass and biochemicals. It is also an area that is emerging in the hydrogen production arena, through the use of bio-feedstocks.

Capture carbon

scale to support the decarbonisation of multiple sectors: heat, transport, heavy industry and power generation. It also ensures efficient system integration in applications where it can use existing gas infrastructure for transport and storage. Carbon capture offers huge potential to neutralise the impact of fossil fuel production and is an area that is advancing in affordability and scale.

Offset emissions

Investigating the benefits of carbon offsetting through carbon markets is only part of an overall reduction strategy. But it does present two opportunities for organisations to approach emissions reduction. One through compliance markets that are operated by government and require companies to account for emissions. The other is carbon offsetting through participation in sustainable projects.

Balance portfolios

Oil and gas majors can’t rely on the status quo given recent market fluctuations and the legislative requirement to reduce emissions. In recent years broader business models are moving organisations increasingly towards power and utilities.